Resilience, Re-Globalization and Emerging Policy Tensions

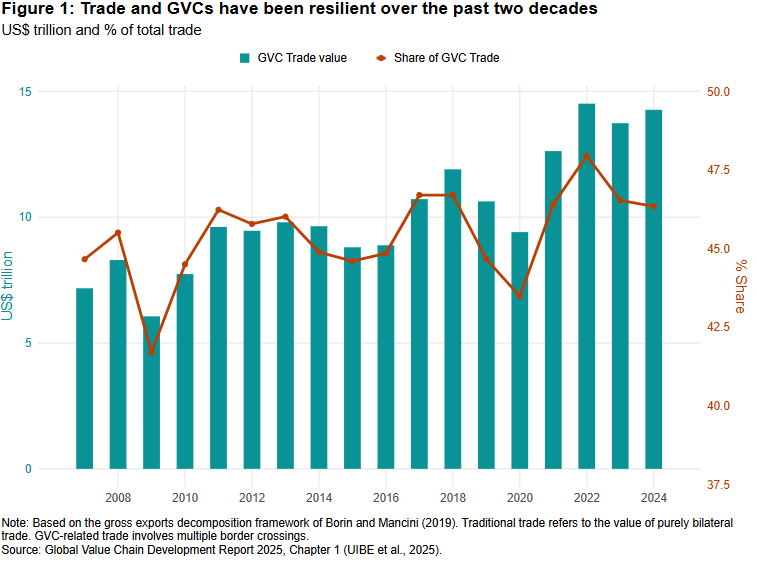

The latest WTO data blog on Global Value Chains (GVCs), based on the Global Value Chain Development Report 2025, challenges narratives of deglobalization. Despite geopolitical tensions, the pandemic shock, financial volatility and climate pressures, GVCs remain central to global trade. In fact, they still account for 46.3% of global trade, only slightly below their 2022 peak (see Figure 1).

Rather than collapsing, GVCs are adapting. They are becoming more digital, more regional, and more shaped by security and sustainability concerns. This evolution reflects structural transformation rather than fragmentation.

Resilience in a Fragmented World

Over the past two decades, international production networks have endured overlapping crises. COVID-19 exposed vulnerabilities, while geopolitical frictions intensified reshoring debates. However, the evidence indicates continuity, not retreat.

Trade integration is broadening geographically. The share of GVC trade accounted for by the ten most integrated economies declined from 76% in 2010 to 64% in 2024. Emerging economies in Asia — including Viet Nam, India and Thailand — have expanded participation as supply chains reorganize. Early signals also point to greater involvement from Africa and Latin America.

Digitalization and Sectoral Transformation

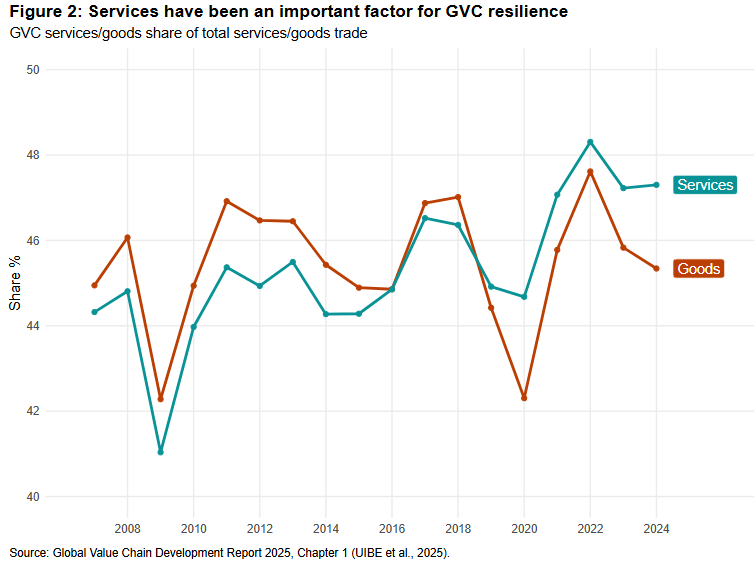

A major shift within Global Value Chains concerns sectoral composition. Historically, GVCs were dominated by goods trade. However, since 2019, services GVCs have gained prominence due to digitalization.

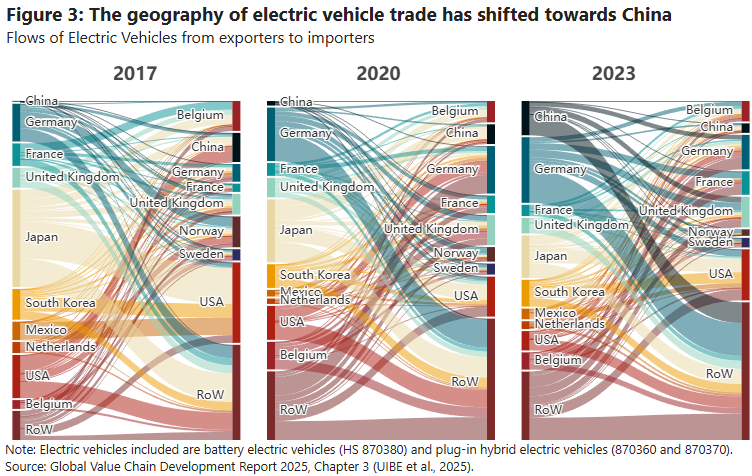

Digital services proved more resilient during COVID-19 compared to goods-based chains (see Figure 2). This structural shift explains part of the stability observed in recent years. Additionally, the electric vehicle value chain illustrates how geography is evolving, particularly with China’s growing centrality in EV trade flows (see Figure 3).

Industrial Policy and Spillover Effects

Government intervention has expanded dramatically. More than 70 economies have introduced targeted industrial and environmental policies, particularly in semiconductors, clean energy and critical minerals.

New empirical evidence shows that indirect spillovers from these policies can equal or exceed domestic effects. While such interventions may support green transitions, they also risk subsidy races and trade distortions if coordination is weak.

The report stresses the need for transparency and policy evaluation to avoid fragmentation.

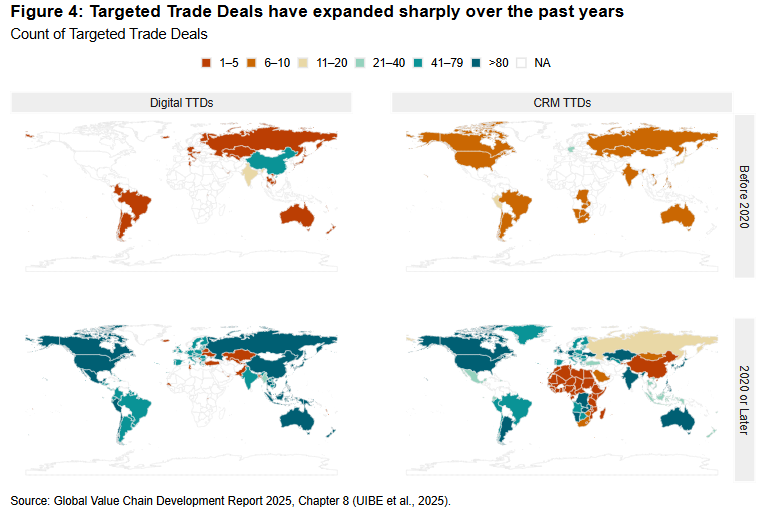

The Rise of Targeted Trade Deals

Another structural development is the rapid expansion of targeted trade deals (TTDs). By 2024, more than 185 TTDs had been signed in digital trade and critical minerals alone. Digital TTD links expanded more than thirtyfold between 2019 and 2024, and 80% of mineral deals were concluded after 2022 (see Figure 4).

Although often non-binding, TTDs appear capable of influencing trade flows. Estimates suggest mineral-related TTDs increased trade values by around 12% between partners.

Overall, the 2025 assessment of Global Value Chains presents a cautiously optimistic message. GVCs remain resilient and adaptive, even as policy intervention, geopolitical competition and security concerns reshape trade patterns. Re-globalization is occurring, not through uniform integration, but through diversification, digitalization and new governance tools.

Still, rising industrial policy activism and overlapping trade frameworks may introduce future volatility. Whether GVC resilience persists will depend on transparency, coordination and the balance between national strategy and multilateral cooperation.

Reference

Stolzenburg, V. (2026, February 25). Global value chains remain resilient amid structural shifts. World Trade Organization Data Blog. https://www.wto.org/