The article Where Rising Climate Risks and Insurance Costs Will Hit Hardest by Manann Donoghoe examines how climate change is driving a climate risk insurance affordability crisis in the United States.

The analysis shows that increasing climate risks are widening the gap between disaster exposure and the ability of households to absorb financial shocks, particularly through the homeowners insurance market.

Climate risk insurance affordability and adaptive capacity

A central concept in the article is adaptive capacity, defined as the ability of households or communities to respond to climate risks. This depends on factors such as income, wealth, homeownership, and financial stability.

The study categorizes U.S. ZIP codes into four groups: adaptable, at risk, vulnerable, and low risk. These categories reflect how climate exposure overlaps with economic resources.

Households with higher adaptive capacity can respond to rising risks by investing in resilience or relocating. In contrast, those with lower capacity are more likely to face increased vulnerability, reduced insurance coverage, or displacement.

Uneven impacts across income and race

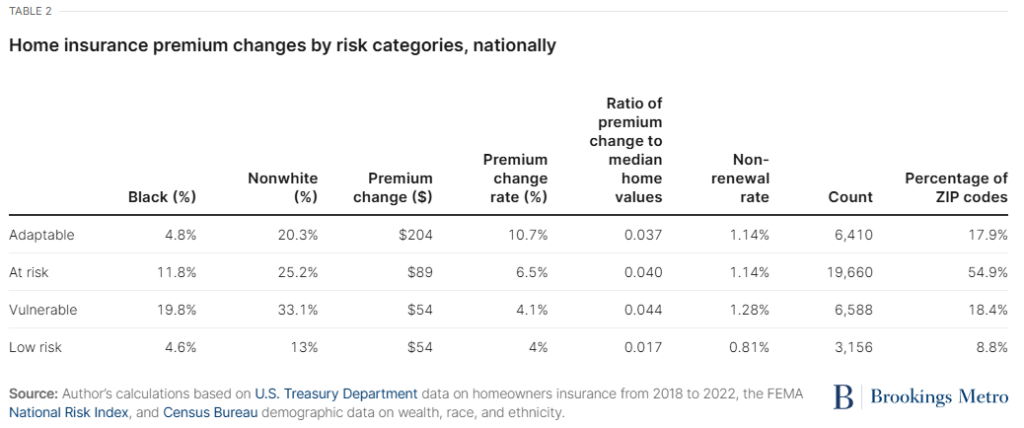

The climate risk insurance affordability challenge is not evenly distributed. According to the data, premium increases are highest in high-wealth (“adaptable”) areas in absolute terms. However, lower-income (“vulnerable”) communities experience a greater relative burden.

For example, as shown in Table 2, premiums in adaptable ZIP codes increased by about $204 on average, while increases in vulnerable areas were smaller in dollar terms but more significant relative to household resources.

In addition, racial disparities are evident. Black and Latino populations are more concentrated in vulnerable and at-risk areas, where insurance instability has a stronger impact. The data also shows that premium increases tend to rise as the share of nonwhite residents increases in a ZIP code.

Policy gaps and future risks

The article emphasizes that insurance market instability is not only a market issue but also a policy failure. Limited federal investment in climate adaptation has shifted the burden of risk management onto households.

Without intervention, the climate risk insurance affordability crisis could deepen existing inequalities in homeownership and wealth accumulation. Insurance alone cannot solve the problem, as it spreads risk but does not reduce it.

The report highlights the need for stronger policies, including investments in climate resilience, improved risk disclosure, and housing reforms that integrate climate considerations.

Reference

Donoghoe, M. (2026). Where rising climate risks and insurance costs will hit hardest. Brookings Institution. https://www.brookings.edu/articles/where-rising-climate-risks-and-insurance-costs-will-hit-hardest/